Sponsored ContentTim LawlessFri 10 Sep 21

Focus on Housing Credit Policies Intensifies

While credit standards remain prudent, higher household debt levels or a further rise in high-debt-to-income ratio lending could be a trigger for tighter credit conditions down the track.

The focus on housing credit policies is becoming more intense as property values continue to rise and mortgage debt levels increase faster than their long-term averages.

It’s rare for the RBA to make a statement these days without including a phrase about the importance of maintaining lending standards for housing loans.

The central bank’s latest statement following its September board meeting was no different and included the line: “Given the environment of rising housing prices and low interest rates, the bank is monitoring trends in housing borrowing carefully and it is important that lending standards are maintained.”

Any tightening of credit policies would likely have an immediate dampening effect on housing markets, the extent to which would depend on the scope and severity of the tighter credit conditions.

Through previous rounds of macro-prudential policies and the Banking Royal Commission, which saw housing credit harder to come by, the impact on housing activity and value growth was clear.

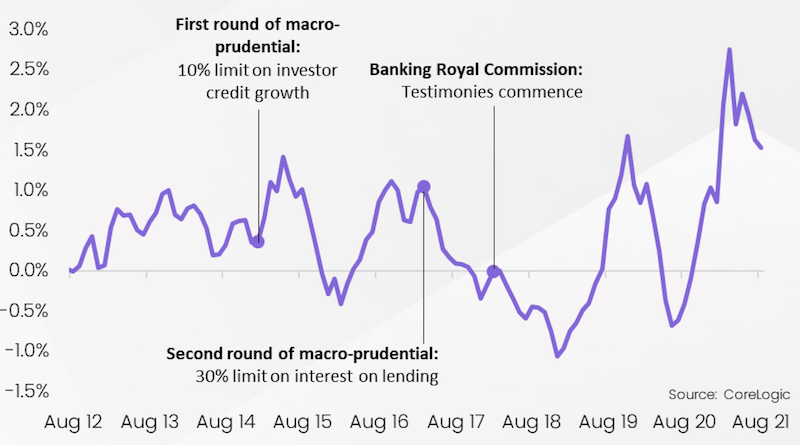

Monthly change in national dwelling values

The first round of macro-prudential policy intervention (announced December, 2014), which involved a 10 per cent speed limit on annual investor credit growth, didn’t make an impact until mid-2015 due to the consultative approach of APRA.

By May 2015 the rate of home value growth had started to reduce, moving into negative territory between November 2015 and April 2016.

The second round of macro-prudential policy announcements came in March 2017, which involved a 30 per cent benchmark on the flow of newly originated interest-only home loans.

The impact of this policy setting was more immediate, resulting in the pace of home value appreciations slowing markedly from the date of implementation. Consequently, national home values declined between late 2017 and early 2018.

Credit policy and home loan serviceability assessments were tightened further through the Banking Royal Commission and housing values again responded negatively.

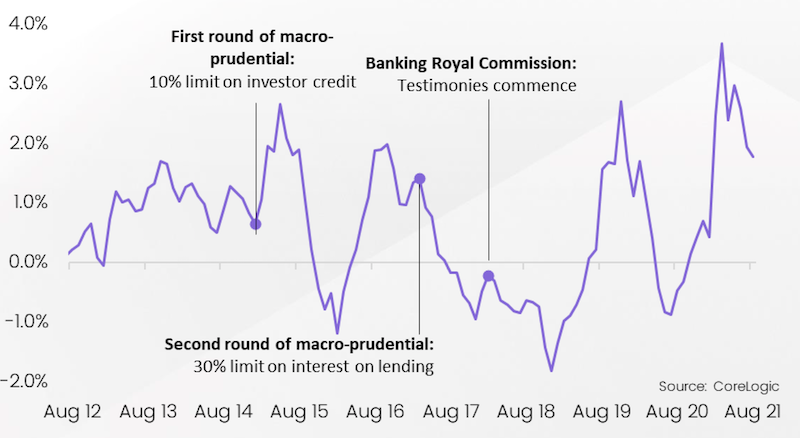

Through each of these periods of credit tightening, the impact on housing trends was more evident in markets that had heightened exposure to the rules.

Sydney, for example, was the epicentre of investment activity, with investors comprising almost 56 per cent of mortgage demand in early 2015.

Housing values in Sydney fell more sharply than the national average during each of these periods of credit policy adjustment as a result.

Monthly change in Sydney dwelling values

In the current environment, the risk for credit tightening is likely to be more focused on overall debt accrual across the household sector rather than investment lending or interest-only lending.

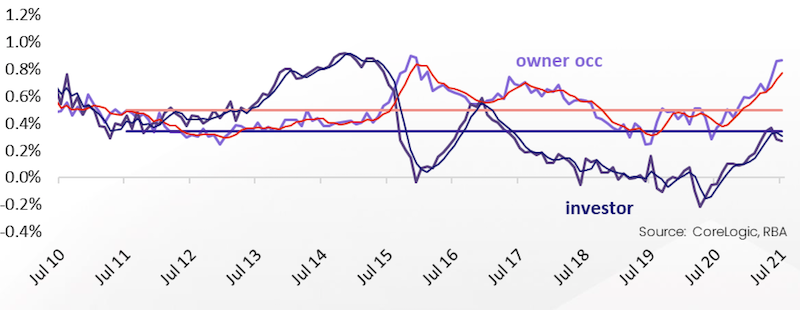

The speed of net investment credit growth (ie: new lending less debt paid down) has increased, but remains below average, and has in fact trended lower over the two months to July, reflecting an appetite for debt reduction across the investment sector.

On the other hand, owner occupier credit growth has been trending higher since June 2020 and has remained above the decade average since November last year.

The proportion of loans being issued with high debt-to-income ratios is another warning sign. The latest data from APRA shows housing loans originated with a debt-to-income ratio greater than six times comprised almost 22 per cent of lending through the June quarter; a substantial lift from a year ago when only 16.0 per cent of new loans had a debt-to-income ratio this high.

RBA housing credit aggregates

Month-on-month change in housing credit, owner-occupier versus investor

Other metrics from APRA for the June quarter were less cautionary. Interest-only lending fell to just 17.2 per cent of housing loans and mortgages with a loan-to-valuation ratio greater or equal to 90 per cent (ie: those purchasers who had a deposit of 10 per cent or less) have been trending lower since December to comprise only 8.6 per cent of new loans in the June quarter.

As the RBA governor highlighted in his testimony to the House of Representatives Standing Committee on Economics last month, the focus from the Council of Financial Regulators, which includes the RBA along with APRA, ASIC and Federal Treasury, is heavily focussed on the sustainability of trends in household borrowing.

A sustained period where household debt grows at a faster rate than incomes implies a build-up of medium-term risks that could trigger a tightening of credit policy.

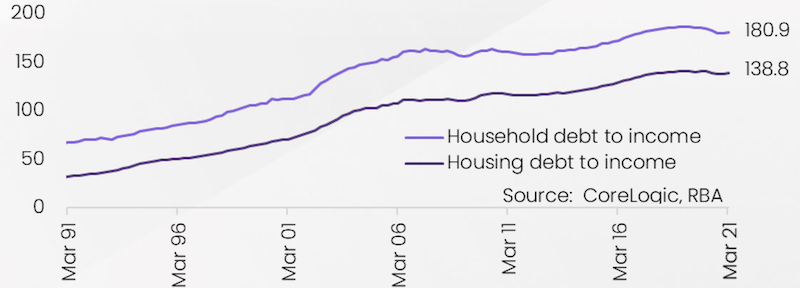

Data on household debt is current to March 2021 and will be updated later this month. The trend shows a subtle reduction in household debt levels since the recent peaks in mid-2019. However, the ratio of household debt to annualised disposable household income did edge higher in March and has likely risen further. Similarly, the housing debt and household debt-to-income ratios also reduced but have recently edged higher.

Considering the pace of growth in housing credit against a backdrop of soft income growth, in all likelihood, household debt, (of which housing debt is the primary component) will be at or close to record highs by the end of 2021.

The likely response to these medium-term risks could be seen in higher serviceability assessments for borrowers—essentially raising the minimum interest rate used when assessing whether a borrower can service their loan, or portfolio level restrictions could be imposed on lenders, probably focused on establishing firm benchmarks on the proportion of high debt-to-income ratio loans that can be issued.

Either of these options would have an impact on credit availability and limit the loan size relative to a borrower’s income or servicing ability.

Ultimately, stricter credit conditions, should they be introduced, would flow through to less home purchasing activity and add to the headwinds of worsening housing affordability, higher levels of newly built supply and stalled overseas migration.

Of course, the tailwind of persistently low mortgage rates and improving economic conditions once lockdowns are eased or lifted will help to keep a floor under housing demand.

The RBA reiterated in their latest statement following the September board meeting that they still expect the cash rate to remain on hold until 2024 at the earliest.

Household debt-to-income ratio and

housing debt-to-income ratio