Sponsored ContentPartner ContentThu 12 Jun 25

Rate Cuts, Residential Rebound Prompts Feasibility Positivity

Residential recovery is on the horizon with election uncertainty and interest rate hikes in the rearview mirror, according to the latest report from JLL.

Head of JLL Residential Project Sales Freya Watson said that the move towards a new cycle had begun.

It will lead to another housing “boom” period, she said, where house prices remain strong and projects are likely to become more feasible.

“With stablising inflation, supply and demand pressures, high rental values, a government focus on the delivery of housing, coupled with continued strong levels of immigration driven by quality of tertiary education, employment opportunities and geopolitical events, Australia is looking very attractive,” Watson said.

Even with considerable constraints, supply is expected to moderately lift in the next few years, according to the latest Decoding Australia’s Residential Market report from JLL.

But what the market will need from developers during this recovery period is worth considering.

Cost bases and strong markets

Financial markets are pricing in a further 110 basis points of interest rate cuts by the end of 2025, taking the official cash rate down to 3.0 per cent.

This may counteract the consistently high interest rates which have increased developer cost bases and severely impacted the feasibility of residential developments.

While banks have been cautious in lending to developers leading to a move to non-bank lenders, a shift is underway, according to JLL.

Banks are now looking more favourably on residential lending, especially in certain markets.

And one of those is the Sydney luxury apartment market.

It has been one of the most consistent in terms of supply, and has remained buoyant against interest rate and construction cost rises compared to the broader housing market in Sydney and beyond.

And it also comes down to demographics, Watson said.

“Downsizers are one of the prevailing reasons high-end sales have remained strong.

“These buyers have benefited from considerable equity growth in existing properties and are generally buying for less than they are selling for,” she said.

Detached home prices, some of which have increased 47 per cent over the last five years especially in premium Sydney suburbs, also mean that buyers are willing to pay a premium to secure high-quality developments in or close to the suburbs where they already live.

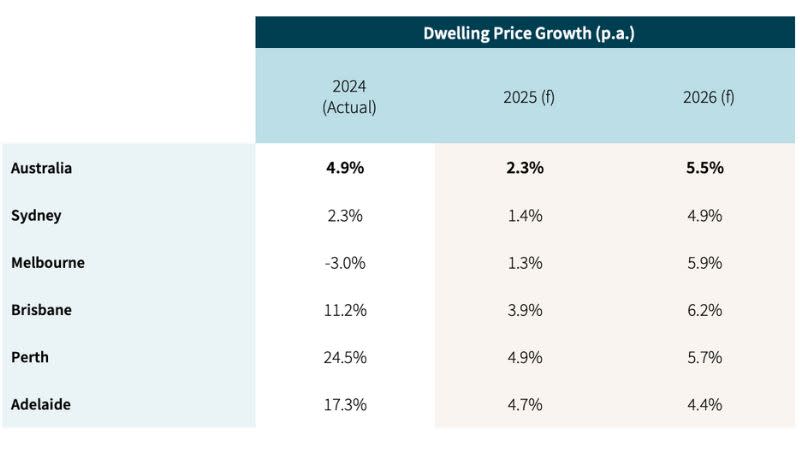

Australian Home Price Forecasts (major banks aggregated)

JLL expects luxury home prices to increase by 7.5 per cent in 2026, compared to a 4.9 per cent growth in all homes.

Perth and Adelaide are expected to continue to outperform in house price growth in 2025, but by 2026 JLL is expecting growth to accelerate across other major capital city markets.

New home supply has not been able to keep up with underlying demand, with an anticipated shortfall of 241,800 homes by the 2029-30 full year.

Return of investors

Investors are returning as we move to a more stable market cycle, Watson said.

“Most investors eventually put their investment apartments on the open rental market once they're finished, adding much-needed new, high-quality rental properties for those looking to rent,” Watson said.

“A steady flow of investor purchases is crucial for meeting rental demand. Without a strong pool of investors ready to put their money into residential assets, we risk worsening the current undersupply of rental properties.”

According to JLL’s report, higher rents and price growth has encouraged investors to return to the market, putting a slow trickle of formerly owner-occupied stock onto the rental market.

While the growth of asking rents has stalled since the second half of 2024, rental vacancy rates have averaged just over 1 per cent nationally since early 2022, and a sudden vacancy rate hike looks unlikely.

Despite this, the owner-occupier market remains strong in Australia, and will only improve with interest rate declines, according to JLL.

What does this mean for developers?

A focus on the owner occupier changes the type and amenities developments need to offer to stay competitive.

“Understanding how people live and what makes a place a desirable place to call home is something that the best-in-class developers strive to achieve regardless,” Watson said.

This means everything from considering the new housing configurations needed for work-from-home to communal spaces and pet-friendly apartments.

But it also means marketing strategies need to change.

“Sales strategies and messaging naturally pivot to speak to owner occupiers directly, as their main drivers do differ to those of an investor, who also require the same fundamental underpinnings but perhaps with less emotional attachment to them,” Watson said.

“Things such as community, access to schooling, local amenity and transport are of primary importance to owner occupiers.”

Read JLL’s Decoding Australia’s Housing Market report >>

The Urban Developer is proud to partner with JLL to deliver this article to you. In doing so, we can continue to publish our daily news, information, insights and opinion to you, our valued readers.