ResidentialEliza OwenThu 08 Oct 20

What Does the Federal Budget Mean for the Australian Housing Market?

Three major housing-related measures were highlighted in Treasurer Frydenberg’s budget address on 6 October: an extension of the First Home Loan Deposit Scheme, additional low-cost financing for affordable housing through National Housing Finance and Investment Corporation and additional funding for the Indigenous Home Ownership Program.

Other measures detailed in the budget papers included a proposed capital gains exemption for granny flats for eligible persons from July next year, and a continuation of funding for state social housing services.

The papers also note that the expansion of the first home loan deposit scheme will be complemented by announced changes to ease credit regulations, which would boost credit availability.

Funnelling new demand into new property

First home owners have previously been a target of demand-side housing stimulus during economic downturns. Currently, Australia may be in a demographic “sweet spot” for first home buyer demand.

The relatively large millennial generation is now estimated to be aged around 26 to 37 years old, and according to ABS data, this puts millennials into the most common first home buyer age groups.

Alongside the typical barriers to entry for hopeful first home buyers, this may be one of the reasons the first home loan deposit scheme has been so well-subscribed since its introduction in January this year.

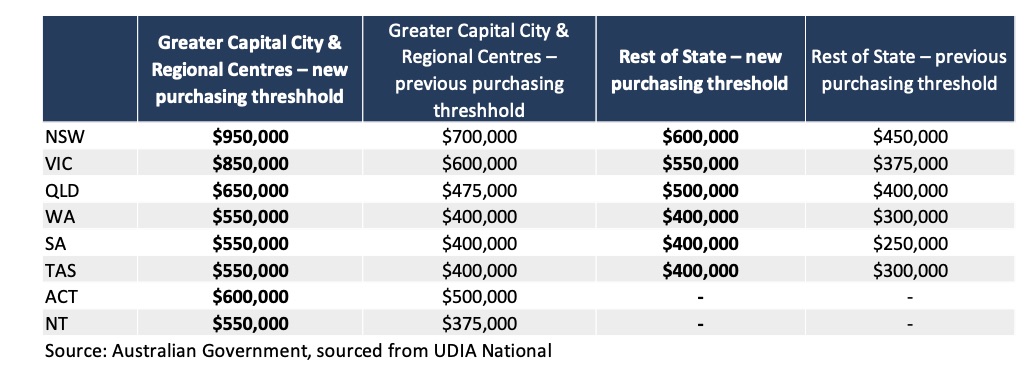

The extension to the First Home Loan Deposit Scheme will see an additional 10,000 places available between 6 October and 30 June 2021, adding to the 20,000 places made available since the scheme started in January 2020.

However, these additional places are for construction or purchase of newly-built homes, and the price thresholds have also been increased for newly built homes, which would potentially further incentivise a pivot away from the established housing market.

The change in purchasing thresholds by region are summarised below.

It will be interesting to see if these conditions create as rapid an uptake as the places for established housing.

In 2008, the temporary boost to the first home owner grant provided added incentives for new builds, yet 85 per cent of its uptake was directed at established housing.

However, incentives limited to new home builds could still help soften the blow to dwelling construction through Covid-19.

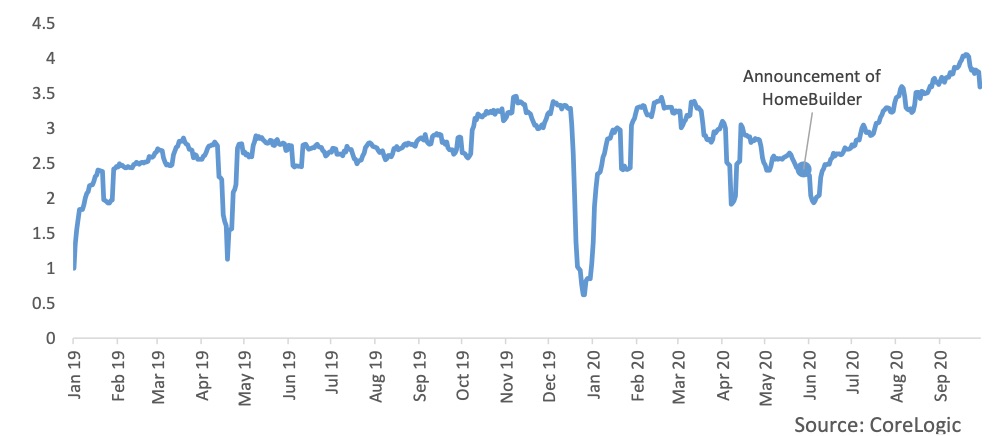

Since the introduction of the HomeBuilder scheme, new home sales have been boosted across Western Australia, South Australia and Queensland.

CoreLogic data shows valuations ordered for the purpose of construction loans have seen a boost above pre-Covid levels since the introduction of the HomeBuilder scheme.

Valuations ordered for construction loans: 7-day rolling count

In terms of the impact these schemes would have on the established market, the increased incentive for new home builds could reduce established home prices if demand is diverted from this sector.

However, the price of newly built homes may rise up to the threshold cut-off.

It is worth noting that despite the rhetoric employed around the extension of the scheme supporting the construction sector, the budget papers highlight that this will not be enough to offset a decline in new dwelling investment.

At August, dwelling approvals for units had fallen -18.4 per cent year-on-year. The budget papers forecast an 11 per cent decline in dwelling investment over 2020-21, before rising 7 per cent in 2021-22.

Indirect Impacts on Housing

With much of this year’s budget focused on the labour market, infrastructure construction and tax cuts, one could be forgiven for

thinking housing reform and stimulus took a back seat in this year’s budget.

However, some of the budget highlights will also have implications for housing. These include:

The JobMaker hiring credit and JobTrainer fund

These initiatives may help re-absorption of young people into the labour force following the initial pandemic-induced shock.

This reflects the disproportionate job loss of young people throughout Covid-19, where around 40 per cent of job losses between March and August were among those aged 24 and under.

Job loss among younger Australians may present less direct risk to the housing market due to their lower likelihood of holding mortgage debt. However, support for youth employment may create more buoyancy in the rental market, where inner-city markets in particular have seen rental income declines since the onset of Covid-19.

A boost to infrastructure spending

Depending on the nature of infrastructure projects, surrounding housing markets could see a rise or fall in demand.

Much of this year’s infrastructure allocation is in roadworks, which can have positive impacts on nearby housing by increasing accessibility to an area, but devalue properties with exposure to high traffic intensity, construction and noise pollution.

Support for regional Australia

The budget outlines $350 million in support for regional tourism to attract domestic visitation, and seeks to strengthen regional industry through concessional loans to farmers and access for exporters to global supply chains.

This may further generate interest in regional dwelling markets, beyond what has resulted from Covid-19 and the normalisation of remote work.

However, it worth noting this budget allocated little to fossil fuel alternatives, with climate

change presenting on ongoing challenge to the liveability of some regional markets.

Beyond the Budget

Further to the budget, there have been many institutional interventions which have likely played a role in stabilising housing market conditions since Covid-19. These include, but are not limited to:

A comprehensive monetary easing package from the RBA, which saw a reduction of the cash rate to 0.25 per cent, bond yield targeting and the establishment of a term funding facility which has been extended to June next year;

Early access to $10,000 of superannuation in 2019/20 and 2020/21;

The Australian Prudential Regulation Authority (APRA) changed capital ratio expectations for the banking sector in March, facilitated home loan deferrals and later extended the availability of deferrals to March 2021;

The availability of JobKeeper and a boost to JobSeeker, which were made available from March, and extended to March 2021, albeit in a tapered form; and

A mix of state-based incentives for home buyers, such as the Building Bonus grant in WA, the Home Improvement Scheme in the NT, and temporary stamp duty discounts in NSW.

These events remind us that housing does not operate in a vacuum. Many different factors are currently supporting housing demand.

This has created a turn in housing market sentiment, which is seeing prices rise across the small capital cities, and a softening of price declines across Sydney and Melbourne.

Looking forward, there may still be more tailwinds to come.

The RBA left the cash rate on hold in October ahead of the budget, but hinted in the final sentence of the statement on the decision that “additional monetary easing” was possible, and a recent address by Deputy Governor Guy Debelle carried the same messaging.

Lower interest rates, together with easier access to housing credit could create further housing market demand, given prices have historically increased against a lower cost of debt and greater availability of housing finance options.