Sponsored ContentPartner ContentThu 15 Jun 23

Tough Time but No Reason to Wipe Out

A macroeconomic situation like this hasn’t been experienced since the 1970’s.

Inflation at record levels, feasibilities under pressure under ever-increasing build costs (if you can get a builder), projects getting shelved, builders falling over, and developers failing to meet funding hurdles.

In this article, STAC Capital managing director Mark Trayner, outlines that even in the dark times, opportunities are to be found.

With banks collapsing overseas and bets on a global recession, international credit markets are again erring towards “risk off”.

Throughout 2021-22, investors and lenders sought highly leveraged deals in their chase for yield—fast-forward to mid-2023, lower risk and capital preservation is now preferred.

But there are a number of shining lights supporting property development.

Record low unemployment and strong immigration will only make the severe housing shortage worse (as well as other sectors such as industrial).

For all the talk about fears in credit markets, there is still plenty of money around.

The question then posed to me, as a property development finance professional is, with all of these challenges, what do developers need to focus on in order to get their projects delivered successfully?

Reflecting on what we’ve seen during the past 18 months in our Brisbane office, among roughly $500m in loans we’ve arranged funding for and invested our own capital in, here’s what we currently consider to be our hot tips.

Higher rates demand greater care

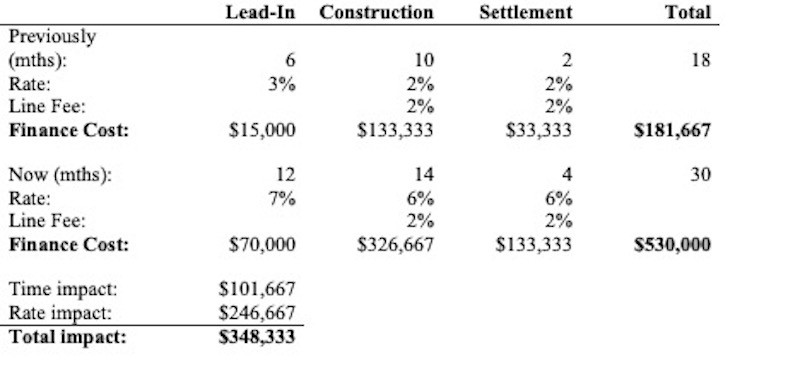

Higher rates alone hurt, but it’s made much worse with timeframes blowing out at all stages—getting approvals, labour shortages and certifications/infrastructure/government and buyer financing.

As an example, if you had a $1-million site acquisition loan, then a $5-million construction loan, here’s how much extra the rate and time costs (and keep in mind this is using cheap bank pricing).

That’s nearly triple the finance cost. Just to add insult to injury, if you had to add $500,000 of mezz due to construction cost increases, finance costs rise to about $680,000—over 10 per cent of TDC – enough to hurt any feaso.

There are two key take-aways from this:

Play carefully with high leverage. High LVRs in a higher rate environment, very early pre-DA, can be dangerous if you’re going to sit on the site for an extended period. However, we are not saying you should not use mezzanine debt or private finance—we are still very actively doing this—but do so ideally when there is greater certainty around timeframes and the feasibility.

Actively manage timeframes. When feasos don’t have a lot of fat, it’s vital to run a tight ship, to be on top of everyone and everything—time is [now a lot of] money!

The bottom line is not the bottom line

Most developers are very good at working the feasibility to drive the bottom-line dollar profit. But many of the best developers actually focus on a different metric: IRR (Internal Rate of Return) on Equity.

Let’s say you had $1 million cash to invest in your next project with a TDC of $4 million, then you rolled the capital and profits into the next project and so on and so on, so that the LVR is always the same (ie: do larger and larger projects). Which option would be better?

Invest it into one project that takes 20 months, with a profit margin of 20 per cent; or

Split the $1 million into three projects ($333,000 in each = only ~8 per cent of TDC), they only take 15 months, but the margin reduces to only 15 per cent and you only get 50 per cent of the profit of each project?

Many developers would scoff at option B, with a lower profit margin and only getting half the profit. But at the end of five years, that $1 million becomes:

Cash equity $5,832,000 = IRR 41 per cent

Cash equity $13,032,000 = IRR 66 per cent.

I put two financing structures into play for this example, which can be used together or in isolation:

Private Finance: higher cost than banks means lower profit margin, but reduced pre-sales hurdles can reduce timeframes, which in turn can allow you to turn your money over faster, doing more projects over the long term. This can also allow you to lock in your build cost sooner, potentially resulting in significant savings (which can make the expensive finance cheap).

Leveraged Finance: which can be by way of profit sharing (Preferential Equity) or Mezzanine Debt, or even just “stretch senior” private finance. By spreading your equity across multiple projects, or doing larger projects than what you would otherwise be able to do, while you’ll make less profit per project than with only bank finance, you can get a much higher Return on Equity overall.

There’s no “blanket best way” to finance projects—our recommendations are always based upon specific situations and the developers’ personal preferences.

The key in our opinion, as with any strategic decision, is to not wear blinkers; at least consider the various potential options and critically compare them, before making a choice as to which is best for you and your projects.

Liquidity over price

When we started STAC Capital in 2017, Australia’s non-bank market was still relatively immature. Most of the players were relatively unknown to anyone not active in the space, so banks were financing the lion’s share of projects.

Fast forward to 2023, we have more than 300 lenders in our database. Every lender has different appetites and capabilities, depending on loan size, asset type, location, gearing limits and where in the capital stack they play.

Some have been doing the same thing non-stop for years, others move their goalposts from time to time.

More recently, the “risk off” global attitude has resulted in goal posts moving. We’ve recently negotiated a few highly leveraged construction deals at around 75 per cent of GRV in the range of $20 million to $50 million; a year ago these would have been highly competitive processes, now they are much more difficult.

Even worse, rumours abound of some funders being on shaky ground because of big deals gone bad and investors withdrawing funds.

In an environment like this, we recommend:

“A bird in the hand is worth two in the bush”—we’ve seen developers scoff at deals because of the cost, only to still be standing around not progressed six months later, so don’t be that guy;

Quality over quantity—it is worth paying a bit more for a lender who has reliable sources of capital, with a reputation of working collaboratively with their borrowers.

Be wary of the salesman

I’ve long ago lost count of how many developers have said they don’t need help with finance because “we have a really solid X-year relationship with our bank”.

Their banker promises they’ll get the deal done, then at the 11th hour—radio silence followed by tail between their legs after a beating from credit, “sorry we’re out”, or at best an LVR miles short of what was promised.

The cost to the developer of this often-unfounded loyalty can be immense—from more expensive 11th hour finance to losing the site and your deposit.

For all the talk of relationships and loyalty, our experience has found that 20-plus-year relationships can amount to nothing when one or two policy boxes aren’t ticked (or when head office changes appetite), yet a completely new lender can be keen to do the deal.

Putting your trust in one banker’s or lender’s promises was, once upon a time, a relatively safe bet; don’t make the mistake of believing that it still is.

Your critical challenge

Amid an economic environment not seen for five decades, with high inflation and increasing building costs, high interest rates and shaky international credit markets, there are still shining lights in property development.

As developers, the critical challenge is to adapt and strategise smartly to survive and thrive. Financial structures can be your friend, they can help you achieve greater results, but not used smartly, they can ruin you.

Manage project timeframes, favour liquidity and risk over price, concentrate on long-term metrics like IRR on Equity rather than merely the bottom-line profit. Finally, be cautious of unfounded loyalty to traditional banking relationships.

Navigating these complexities isn’t easy; it demands not just industry knowledge but also an adept understanding of finance and strategic planning.

That’s where STAC comes in. With our decades of experience in development finance, including structured finance across the entire capital stack and just about every asset class, we can provide strategic support no matter how simple or complex your pipeline.

Don’t let the current economic climate curb your ambition. Reach out to us and let’s turn these challenges into opportunities together.

The Urban Developer is proud to partner with STAC Capital to deliver this article to you. In doing so, we can continue to publish our daily news, information, insights and opinion to you, our valued readers.