ResidentialLeon Della BoscaThu 01 May 25

Adelaide Overtakes Perth as Property Prices Hit New Peak

The Australian property market last month continued its upwards trajectory as national home prices reached a record high.

This is despite the pace of growth “moderating” compared to earlier months, according to the PropTrack Home Price Index for April.

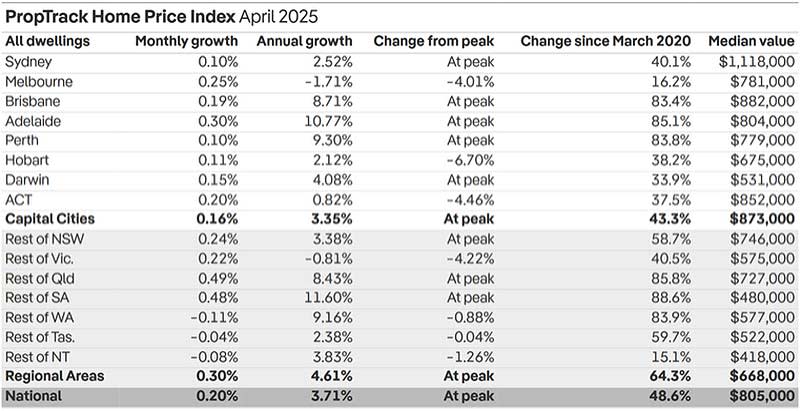

National median home prices increased by 0.2 per cent in April to reach $805,000, a 3.71 per cent rise on the same period last year.

The data reveals a shift in growth patterns across capital cities, with Adelaide emerging as the strongest performer.

The SA capital has overtaken Perth for the highest annual growth rate, recording a 10.77 per cent increase year-on-year. Perth followed closely with 9.3 per cent.

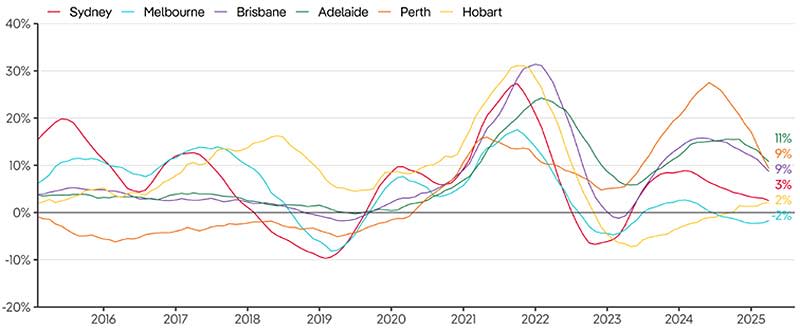

This is a shift from late 2024 when, according to Domain’s House Price Index, Perth was leading the nation with annual growth near 19.5 per cent.

The latest PropTrack data aligns with other recent property reports showing sustained strength in midsized capitals despite broader market moderation.

CoreLogic data from earlier this year showed that Adelaide had begun to outpace Perth in quarterly growth as early as December of 2024, a trend that has now extended to annual figures.

Regional areas outpaced capital cities in April, with values climbing 0.3 per cent over the month to sit 4.61 per cent higher than a year ago.

Since March 2020, regional property prices have surged by 64.3 per cent, significantly outperforming the 43.3 per cent growth seen in capital cities over the same period.

REA Group senior economist and report author Anne Flaherty said, “While national home prices rose in April, the rate of growth has slowed compared to the first three months of the year”.

“Should interest rates fall in May, we may see the rate of growth pick up again as borrowing capacities increase and mortgage repayments decline.”

The report highlights an emerging trend of convergence in growth rates across previously divergent markets.

“The rate of price growth is moderating in outperforming cities such as Perth, Adelaide and Brisbane, while underperformers such as Melbourne, Canberra, and Sydney have started to pick up,” Flaherty said.

This pattern mirrors market behaviour observed in late 2024 and early 2025, when the February interest rate cut—the first in four years—provided a modest boost to previously underperforming markets while growth in the strongest capitals began to moderate.

Annual change in home prices, by capital city

All capital cities recorded price growth in April, with Adelaide and Melbourne leading at 0.3 per cent and 0.25 per cent respectively, while Sydney and Perth recorded more modest gains of 0.1 per cent each.

Housing affordability remains a key issue ahead of the upcoming federal election, with both major political parties announcing incentives for first-home buyers.

Many potential buyers appear to be waiting on these policy initiatives before entering the market.

“Whichever party is elected, the combination of increased first home buyer incentives, lower interest rates, and supply side challenges are expected to contribute to even higher property prices in 2025,” Flaherty said.

The report reveals differences in performance between property types, with houses showing stronger monthly growth than units (0.24 per cent versus 0 per cent), though units slightly outperformed houses in annual growth terms (3.88 per cent versus 3.67 per cent).

Regional Queensland and South Australia emerged as the top performing regional markets in April, with growth of 0.49 per cent and 0.48 per cent respectively, reinforcing the continued strong performance of markets outside major metropolitan areas.