‘Surprisingly Weak’ Building Activity Rounds Out Horror Year

A substantial fall in building activity for the December quarter does not appear to bode well for the coming year.

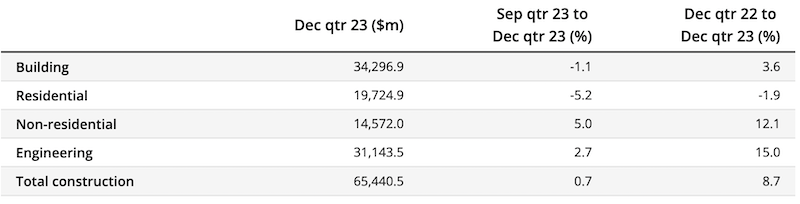

Preliminary data from the ABS shows residential building activity fell 5.2 per cent quarter-on-quarter to $19.72 billion (chain volume measure) in seasonally adjusted terms for the last quarter of 2023.

This was a surprisingly weak figure, pointing to the heavy weight of capacity constraints, Oxford Economics Australia economist Michael Dyer said.

“Trade labour shortages in particular are persisting,” he said.

“Construction industry job vacancies remain elevated, around double their long-run average, while about a quarter of construction firms are reporting vacancies.”

The value of total construction work done rose 0.7 per cent in the December quarter, in seasonally adjusted terms.

The increase was driven by engineering work, which rose 2.7 per cent in the December quarter, 15 per cent higher than the same time last year.

Building work done fell 1.1 per cent for the quarter, but was still 3.6 per cent higher than the same period last year.

Dyer said bottlenecks continued towards the back-end of the construction process, slowing the rollover on to new projects and contributing to the housing supply challenges.

“The volume of houses under construction turned in the third quarter of 2023, falling below 100,000 for the first time since September 2021, however this is still around 50 per cent above the long-run average,” he said.

Value of construction work done, chain volume measures

“Meanwhile, higher interest rates, delays and cost escalation are weighing on new home demand.

“Nonetheless, an elevated backlog of work has built up over the prior two years and efforts to clear this will inevitably place a floor under activity in 2024.”

Non-residential building held up over the final quarter of 2023, lifting 5 per cent, with non-residential work done reaching $56.02 billion for the calendar year, up 7.3 per cent on the prior 12 month period.

“Private investment took a step up, while support continues to arise from a sizeable pipeline of public works already under way,” Dyer said.

“The lead from non-residential approvals continued to soften from recent record highs in December, with momentum stalling for lower value commercial fitout projects in particular.

“The increased level of detachment between approvals and commencements remains, which we anticipate will persist near term and begin to drag as the current backlog clears.”